Daily Market Outlook, August 12, 2022

Overnight Headlines

- UK Economy Contracts Slightly Less Than Feared At 0.6%

- Fed’s Daly: Base Case Is 50Bps Hike In September, Open To 75Bps

- Biden Plots A 2024 Presidential Run — And A Trump Rematch

- EU Proposes Significant Concession To Iran To Revive Nuclear Deal

- China To Partially Renew Medium-Term Policy Loans, Keeping Rate Steady

- Shanghai Finds First Covid Cases In Week; Hainan Stays Elevated

- RTRS POLL: Japan July Core CPI Seen Rising 2.4%, Near 8-Year-High

- Japan PM Kishida Pledges New Steps To Deal With Rising Fuel, Food Prices

- New Zealand’s Manufacturing Activity Expands In July

- Australian, NZ Dollars Buoyed By Softer Federal Reserve Hike Views

- Yields Soar In Australia And NZ As World Rethinks Slower Rate Hikes

- Oil Prices Slip On Cloudy Demand Outlook, But Poised For Weekly Gain

- German Chancellor Scholz Backs Proposal For New European Gas Pipeline

- Asia Stocks Mixed, Japan Stocks Outperforming As US Yields Dip Slightly

The Day Ahead

- Equities across the Asia Pacific are mostly trading higher with most major indices in the region set to end the week up. Sentiment has been buoyed by prospects of less aggressive interest-rate increases from the US Federal Reserve. However, comments overnight from US Fed member Daly said that further interest rate increases were still warranted, albeit noting that the welcome news from the July US CPI report may mean that a 50bp interest rates increase is more appropriate than another 75bp rise.

- Just released UK GDP data showed the economy contract by 0.1% in Q2, largely due to a 0.6% m/m decline in June activity on account of the double Jubilee bank holiday.

- The past few days have seen some welcome news on the US inflation front. Most notably, on Wednesday, the latest US CPI print, saw the headline rate drop from 9.1% in June to 8.5% in July, softer than market expectations of a fall to 8.7%, while the ‘core’ rate confounded expectations of a rise to 6.1% and printed unchanged at 5.9%. Yesterday’s Producer Prices report for July, meanwhile, also printed below expectations with both the headline and ‘core’ rates, pulling back more sharply and pointing to some ‘unanticipated’ easing in pipeline price pressures in the US manufacturing sector. The softening in inflation pressures seen in both reports primarily reflected the recent fall in the oil price, but there were also some signs that an easing in supply bottlenecks may also be pushing down on goods price inflation more generally. However, given indications that domestic pressures are pushing up services inflation the Fed will probably want much more evidence before it changes course on monetary policy. More importantly for the US Fed, will be how these developments are impact upon inflation expectations.

- Later today, the University of Michigan will be releasing its preliminary estimate for July US consumer sentiment, which is expected to show a modest improvement from 51.5 in July to 52.0 this month on account of the recent fall in gasoline prices. The report will also provide a gauge on US consumers’ expectations for inflation 1yr ahead and 5-10yrs ahead. The reading for the latter fell 0.2% points in July to 2.9% but the distribution remained wide, pointing to ongoing risks that inflation expectations could de-anchor. While the 1yr ahead measure is expected to moderate further, on account of the recent decline in gasoline prices, the greater focus will be on the 5-10yr measure for signs on how longer-term inflation expectations are reacting to recent trends in inflation, although the downside surprise in the July CPI report is likely to have come after the cut-off date for today’s reading.

- Elsewhere, it is a quiet day for economic data releases with no major reports due in the UK. For the eurozone, the latest industrial production report is due at 10:00 (BST). On balance, already-released regional reports from Spain, Italy, Germany and France have been better than expected and point to upside risks to the market consensus expectation of 0.2% rise

FX Options Expiring 10am New York Cut

- EUR/USD: 1.0050-55 (2.11BLN), 1.0200-05 (1.2BLN)

- 1.0225-30 (675M), 1.0265 (326M), 1.0300-10 (2.86BLN)

- 1.0325 (814M), 1.0350 (841M), 1.0400 (410M)

- USD/JPY: 133.98-00 (1.61BLN), 135.00 (266M), 135.45 (300M)

- GBP/USD: 1.2100 (462M), 1.2300 (576M)

- USD/CHF: 0.9400 (325M), 0.9550 (260M), 0.9700 (300M)

- AUD/USD: 0.6950 (358M), 0.7100 (689M)

- USD/CAD: 1.2700 (1.45BLN), 1.2795-00 (1.1BLN)), 1.2850 (311M)

- 1.2975 (425M)

Technical & Trade Views

EURUSD Bias: Bearish below 1.0410

- Steady after leading the USD lower on Thursday, closing up 0.25%

- EUR was stronger across the board, EUR/JPY +0.35%, EUR/GBP +0.4%

- Little news, so EUR strength likely short covering in thin summer markets

- 1.0300/05 2.62 BLN. 1.0325 700mln and 841 mln 1.0350, Friday’s close strikes

- Resistance 1.0410, support 1.0290

- 20 Day VWAP bullish, 5 Day bullish

GBPUSD Bias: Bearish below 1.23

- Heavy in Asian trade but signals remain constructive

- -0.2% after closing -0.1%, capped by EUR/GBP demand, cross closed +0.4%

- BoE – weakening regulators would undermine market reforms

- Drought could be the next hurdle for the UK economy

- Offers sited at 1.2280/1.23 bids 1.2060

- 20 Day VWAP is bullish, 5 Day bullish

USDJPY Bias: Bearish below 136

- Touch firmer, as Fed policy expectations lead

- +0.2% at 133.30 amid a 132.89-133.50 range – USD firmer on Fed comments

- Fed’s Daly, 50pt September hike “makes sense”, but open to 75pt

- Foreign investors net buyers of Japan shares for last week

- USD may settle in broad 130.00-135.00 range ahead of Jackson Hole Aug 25-27

- Bears target a test of 130

- Offers seen at 136.20

- 20 Day VWAP is bearish, 5 Day bullish

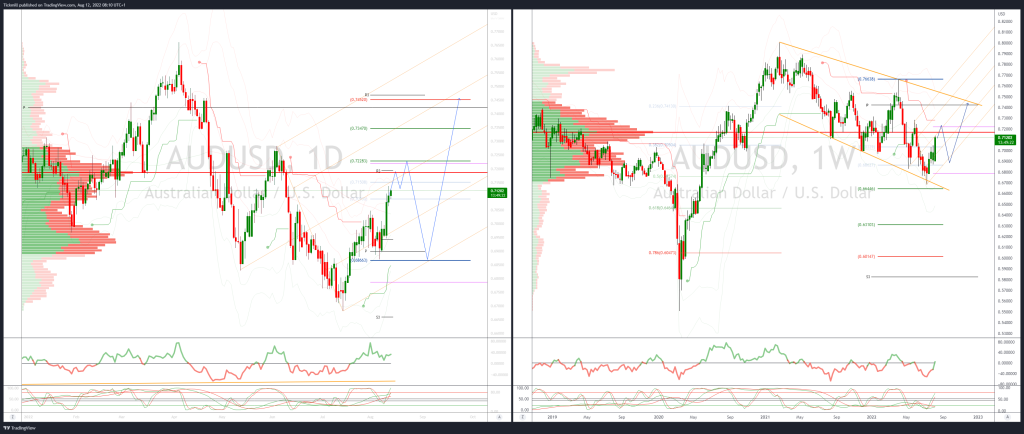

AUDUSD Bias: Bullish above .7050

- Recovers from early dip in quiet Asian session

- AUD/USD opened +0.34% at 0.7104 after trading as high as 0.7136

- It dipped to 0.7090 early Asia when USD firmed and AUD/NZD was sold

- Buyers emerged and it firmed to 0.7105/10 heading into the afternoon

- Offers eyed .7270/30, bids .7040’s

- 20 Day VWAP is bullish, 5 Day bullish

BTCUSD Bias: Bearish below 25.3K

- Bitcoin fails at key chart pivot; bulls may lose confidence

- BTC turned south late Thurs, flashing warning light to bulls

- Ended tad lower for the day after rising as much as 4.0%

- UNable to capture pivotal 25k level

- If it ends Fri below sub 24k, will exit uptrend channel

- Fed’s Daly says 50bps is her base case for Sept

- Bulls need a close above 25k to gain significant upside momentum

- Closing below 21k would be a noteworthy downside development

- 20 Day VWAP is bullish, 5 Day bullish

Source: Tickmill