Daily Market Outlook, February 1, 2023

-

Markets Await Fed Decision, After A Buoyant Month End Close on Wall Street

-

Asian equity markets took the positive impetus on Wall Street and opened higher, driven by month end mark ups on US stocks with the benchmark SP500 closing +1.46% at 4,076, leading Asian investors to follow suit, bidding up equities with the Japanese benchmark Nikkei briefly breaching the 27k level on the upside, both the Shanghai Comp and Hang Seng carved out meagre gains, although the upside was contained as the Caixian Manufacturing data delivered a sixth consecutive month of declines, dampening investor appetite.

-

European investors will eye manufacturing PMI data for both the Eurozone and the UK, these are second readings, while they are expected to show modest upticks both remain entrenched in contractionary territory, below the pivotal 50 level representing expansion. In the UK house price data released this morning surprised to the downside printing 1.1% versus a 1.9% expected and down from the prior 2.8%, this represents a net 3.2% decline in prices from the August peak last year, this only adds to the sombre mood in the UK as the country faces its largest day of strike action of the winter, with severe disruption to the rail network, school and the public sector. The main data of note for the Eurzone will be this morning CPI print which is expected to show a second consecutive monthly decline, the mixed messages from Spanish and French readings coupled with the postponement of the German release is likely to leave the ECB with little excuse to deviate from the anticipated 50bps move at Thursday’s meeting.

-

In the US, investors eagerly await the official policy announcement this evening, markets are braced for the eighth consecutive rate increase, however, it is also expected that this move will be a 25bps hike, representing the second slow down in rate increases. Investors will parse comments from Fed Chair Powell during his press conference, equity bulls will be looking for language that suggests the Fed feel they are on course to deliver a soft landing for the economy, hence, a lower terminal rate in sight would be well received by markets, however, the concern is that the Fed Chair will be unnerved by an apparent loosening in financial conditions give the strong start to the year in global equity markets, he may look to guide ‘higher for longer’ remains the anchor for the committee, certainly he will look to talk down any belief of rate cuts later in the year. Ahead of the FOMC decision markets will receive January ISM manufacturing data which may deliver a fourth monthly decline, with another sub 50 print expected.

-

Markets-wise, European bourses, FTSE & EuroStoxx are opening flat, US futures are also trading with a neutral tone as investors await a round of risk events, as well as the central bank risk ahead, investors will also receive a number of significant earnings reports in the coming days with Meta, Apple, Amazon and Google all set to report, which will be capped off on Friday with the all important Non Farm Payroll release.

Overnight News of Note

-

Asian Stocks Rise And US Futures Waver Before FOMC Decision

-

Dollar Pauses Ahead Of Fed Rate Decision

-

Oil Rises As US Recession Fears Ease And Dollar Slips

-

Nasdaq Logs Best Jan Since 2001 As Stocks Climb To Cap Off Stellar Month

-

China’s Jan Factory Activity Contracts At Slower Pace Amid Infections

-

RBA’s Head Economic Analyst: We Believe Peak Of Inflation Was In Q4

-

New Zealand Q4 Jobless Rate Edges Up To 3.4%, Just Above Historic Lows

-

Fed Is Expected To Slow Rate Hikes In Signal That Work’s Not Over

-

US Says Russia Violated Nuclear-Arms Treaty By Blocking Inspections

-

UK And EU Reach Post-Brexit Customs Deal For Northern Ireland

-

Inflation In UK Shops Hits A Record Despite Broader Easing

-

Nasdaq Logs Best Jan Since 2001 As Stocks Climb To Cap Off Stellar Month

-

AMD Rev Beats Targets, Wall St Relieved After Intel’s Grim Outlook

-

Amgen Revenue Falls Slightly As Lilly Covid Deal Contributes Less

-

Mondelez Beats Quarterly Sales Estimates On Resilient Snack Demand

-

Intel Cuts Pay Across Company To Preserve Cash For Investment

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

Options Expiration For the New York Cut 10am EST

(BOLD expiries with a value of a Billion+ more magnetic if price is within the daily trading range – source DTCC)

-

EUR/USD: 1.0910 (458M).

-

USD/CHF: 0.9100 (250M)

-

USD/JPY: 129.20 (200M).

-

USD/CAD: 1.3400 (240M)

-

AUD/USD: 0.7140 (302M) 0.7185 (918M)

-

EUR/AUD: 1.5600 (589M).

-

EUR/GBP: 0.8650 (401M), 0.8700 (298M)

CFTC Data As of 27/01 ( Source Reuters)

-

USD net spec short in the Jan 18-24 period; $IDX -0.46%

-

EUR$ +0.86% in period, specs buy 7,365 contract long now +134,349

-

$JPY +1.56% in period yen short cut by 1,326 contracts now -21,635

-

GBP$ +0.44$ in period, short reduced by 763 contracts to -23,934

-

CAD specs -3,453 contracts now -30,712; AUD specs +449 contract now -33,171

-

BTC +7.45%, spec short increased by 810 contracts now -1,437

-

Next week’s data likely mooted by Fed, ECB, BoE meets Feb 1-2 after period closes

Technical & Trade Views

SP500 Bias: Intraday Bullish Above Bearish Below 4040

-

Primary support is 4000

-

Primary objective is 4138

-

Below 3950 opens 3884

-

20 Day VWAP bullish, 5 Day VWAP bullish

EURUSD Bias: Intraday Bullish Above Bearish below 1.0820

-

Primary support is 1.0750

-

Primary objective is 1.10

-

Below 1.0730 opens 1.0610

-

20 Day VWAP bullish, 5 Day VWAP bearish

GBPUSD Bias: Intraday Bullish Above Bearish below 1.2230

-

Primary support is 1.2180

-

Primary objective 1.2460

-

Below 1.2150 opens 1.2100

-

20 Day VWAP bullish, 5 Day VWAP bearish

USDJPY Bias: Intraday Bullish above Bearish Below 131.50

-

Primary resistance is 132.30

-

Primary objective is 125.00

-

Above 133.00 opens 135.00

-

20 Day VWAP bearish, 5 Day VWAP bullish

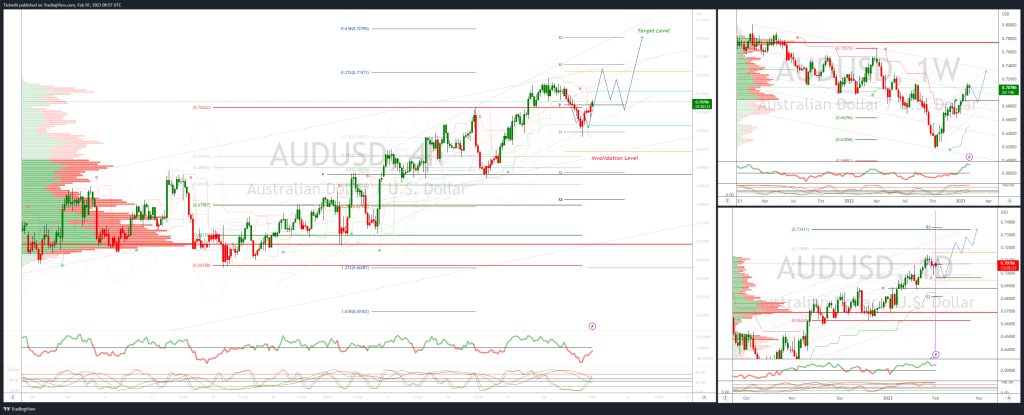

AUDUSD Bias: Intraday Bullish Above Bearish below .6990

-

Primary support is .6940

-

Primary objective is .7250

-

Below .6930 opens .6870

-

20 Day VWAP bullish, 5 Day bearish VWAP

BTCUSD Intraday Bias: Bullish Above Bearish below 22100

-

Primary support 21400

-

Primary objective is 25000

-

Below 21000 opens 20300

-

20 Day VWAP bullish, 5 Day VWAP bearish

Source: Tickmill