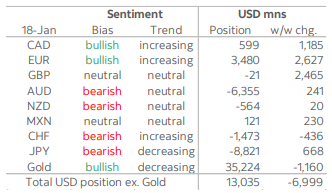

Daily Market Outlook, January 24, 2022 Overnight Headlines Renewed Downturn In Japanese Private Sector Activity In Jan – PMI Australian Private Sector Output Shrinks Amid Covid-19 Hit – PMI Fed Expected To Back First Pandemic-Era Interest Rate Rise In March Goldman Sees Risk Fed Will Tighten At Every Meeting From March ECB’s Holzmann: Euro Area Inflation Outlook Highly Uncertain ECB’s Rehn: ECB 2023 Rate Hike ‘Logical’ If No New Disruption ECB’s Makhlouf Sees Inflation Slowing, No Rate Hike In 2022 U.K. PM Johnson Faces Week That Defines His Political Future Iran Nuclear Agreement Unlikely Without Release Of U.S. Prisoners Yuan Hits 3-1/2-Year High On Heavy Holiday Demand, PBOC Guidance Cryptocurrency Meltdown Erases More Than $1 Trillion In Value Treasury Yield-Curve Mavens Are Pining For Guidance From Fed Oil Climbs On Outlook For Rising Demand As Omicron Wave Fades Asia Shares Tense As Federal Reserve Looms, Ukraine A Concern Cathay Pacific To Post Narrower-Than-Expected 2021 Annual Loss Infineon Sees End Of Microchip Shortage In 2023 – Autmobilwoche Activist Hedge Fund Trian Partners Builds Stake In FTSE 100’s Unilever Activist Investor Blackwells Capital To Call On Peloton To Fire Its CEOThe Week Ahead Fed meets, U.S. earnings due as markets wobble… The highly anticipated Federal Open Market Committee meeting concludes on Wednesday and the market will pay close attention to how worried the Fed is over rising inflation and how aggressive they will be in trying to contain it. There was a lot of chatter early last week suggesting the Fed would start softening the ground for a 50-basis-point rate hike at their March meeting to get ahead of the inflation curve. The speculation spurred a surge in U.S. yields, but it also sent risk assets spiraling lower. The big fall in certain sectors of the equity market cooled expectations the Fed would signal a jumbo rate hike and further rattle risk markets. The Fed will likely signal rate hikes are coming, but they may temper expectations of aggressive action and point out that more improvement in the labour market is needed first. Wall Street rocked lower last week and there will be a lot of attention on upcoming company earnings reports, with heavyweights such as Caterpillar, 3M, Apple, Microsoft, IBM and Tesla reporting. The Nasdaq has fallen over 15% from the highs and is off to its worst 14-day start of the year since 2008.Wall Street rocked lower last week and there will be a lot of attention on upcoming company earnings reports, with heavyweights such as Caterpillar, 3M, Apple, Microsoft, IBM and Tesla reporting. The Nasdaq has fallen over 15% from the highs and is off to its worst 14-day start of the year since 2008. U.S. GDP and PCE dominate global data calendar U.S. fourth-quarter advance GDP will be released this week, with expectations of 5.4% annualized growth after 2.3% in the third quarter. The other leading data release from the U.S. will be the Fed’s favourite inflation gauge, the core PCE price index. Other U.S. data includes durable goods, consumer confidence, University of Michigan sentiment, Markit flash PMIs, and a raft of housing data. Key data out of Europe includes German Ifo and Q4 GDP, euro zone flash PMIs and consumer confidence. Flash PMIs will be the only data of note out of the UK this week. In China, industrial profit data are expected, along with the NBS PMIs and Caixin manufacturing PMI on Sunday, ahead of the week-long Lunar New Year holiday. Japan’s main releases are flash manufacturing PMI and Tokyo CPI. Australia will be releasing CPI and PPI data, with the focus on the trimmed and weighted mean CPI measures. The Reserve Bank of Australia meets on Feb 1 and the CPI data may influence how hawkish their message will be. The NAB business survey is also out this week. CPI data is due in New Zealand as well, along with trade data. Canada has a central bank rate decision.CFTC Data This week’s snapshot for FX market sentiment and positioning reveals a quite significant reduction in broader USD bullish sentiment, with the aggregate USD long position that has accumulated in recent weeks slashed by USD7bn through Tuesday. This is one of the largest 1 week drawdowns in long USD positioning since mid-2020 by our reckoning. The overall USD long position now stands at a little over USD13, the lowest bull bet on the USD since mid-September. Investors were gripped with a sudden (and perhaps short-lived, given subsequent developments) burst of enthusiasm for the EUR last week as spot EUR showed some fleeting strength and tested levels near 1.15. Speculators added some USD2.6bn in net EUR longs as gross longs rose and gross EUR shorts were covered in response to the EUR gains. A sizeable GBP net short in the prior week’s data was cut by a similar amount (USD2.4bn), taking overall risk here back to basically flat. Investors added (slightly) to net MXN longs and (a little more significantly) to net CAD longs, contributing somewhat to pressure on the USD. Modest, offsetting moves were seen in the JPY, where net shorts were reduced USD668mn in the week and, to a lesser extent, in the AUD where record net shorts were pared slightly – USD241mn. Net CHF shorts were lifted USD436mn, in a further sign of respite for the USD. Positioning in the NZD and was little changed. While CAD positioning tilted modestly bullish this week, sentiment has been running negative on the CAD for a number of weeks. Net positioning is relatively mild and—if correct if the Bank of Canada is about to unleash a quite significant round of monetary tightening, positioning has room to expand in the weeks ahead.G10 FX Options Expiries for 10AM New York Cut(Hedging effect can often draw spot toward strikes pre expiry if nearby (P) Puts (C) Calls )USDJPY – 114.90/115.00 466m. 114.70/80 552m. 113.90/114.00 795m. 110.20 550m.EURUSD – 1.1400/20 640m. 1.1290/1.1300 654m. 1.1250/60 414m. 1.1230 876m.AUDUSD – 0.7220/30 1.83bn (1.11bn C). 0.7200 886m. 0.7090/0.7100 455m.CADJPY – 90.50 400m.USDCNH – 6.36 500m.Technical & Trade ViewsEURUSD Bias: Bearish below 1.15 Bullish above EUR/USD opened 1.1350 after rising 0.27% on Friday when US yields eased The opening price was the high and EUR/USD edged lower through the morning Heading into the afternoon it is at the session low at 1.1332 EUR and JPY both eased in Asia as risk currencies had a modest rebound EUR/USD support is at a trend-line at 1.1286 with bids ahead of 1.1300 Resistance is at 10-day MA @ 1.1375 and break would increase upward pressure EUR/USD will likely consolidate ahead of FMC decision on WednesdayGBPUSD Bias: Bearish below 1.36 Bullish above. GBP heavy after falls Friday, awaiting London Cable heavy in Asia, 1.1347-62 after fall to 1.3546 Friday Risk off market mood, weak UK retail sales, lower Gilt yields cited On hold for now just above descending 100-DMA below at 1.3539 Could fall tad lower to @1.3520, 1.3528-30 double bottom Jan 7-10 Likely heavy on rallies still towards 1.3572 hourly GBP/JPY 153.93-154.48 in Asia after fall to 153.85 Fri, short-covering Support from 153.62 daily Ichi kijun, cloud 151.42-153.57 below EUR/GBP buoyant, 0.8358-59 in Asia after rally to 0.8376 Friday E355 mln in 0.8460 strike option expiries today at NY cut GBP bias likely to remain down into upcoming central bank meetingsUSDJPY Bias: Bullish above 114.50 Bearish below Market risk mood still on sour side, JPY better bid across board Nikkei off 1%+ early but some losses recouped, now -0.4% @27,405 USD/JPY tracks away from 113.60 EBS low Friday, Asia 113.65 to 113.93 Heavy from ahead of 114.00, $796 mln option expiries 113.95-114.05 help Tokyo importers, some investors, specs noted on bid into/post-Tokyo fix Supports include 113.52-87 daily Ichi cloud, cushion, 113.28 100-DMA Some bounce in US yields supportive, Treasury 10s @1.773%, Fri low 1.733% EUR/JPY 128.94-129.15, GBP/JPY 153.93-154.48 and AUD/JPY 81.44-83 All see some bounce from Fri lows but caution ahead of spate of CB meets AUD/JPY above 81.40 daily Ichi cloud base, some 82 option expiries todayAUDUSD Bias: Bearish below 0.7250 Bullish above AUD/USD opened 0.7174 after falling 0.76% Friday when Wall Street slumped The mood was a bit brighter in Asia as the E-minis rose 0.75% AUD/JPY moved up around 0.35% to retrace some of the 1.0% drop on Friday AUD/USD traded as high as 0.7187 and was around 0.7185 into the afternoon Resistance is at former trend-line support at 0.7190 where sellers tipped More resistance is at 0.7218 where the 10 & 21-day MAs converge Support is at the 50% retracement of the 0.6994/0.7314 move at 0.7154 View Fed may tone down hawkish rhetoric at Wednesday’s FOMC may calm markets AUD/USD may see some volatility after tomorrow’s Aus CPI

Source: Tickmill